It has been suggested that those lacking access to a bank account, and the financial system more generally, could drive proportionately greater cryptocurrency adoption over people in advanced economies who already have access to financial services.

A paper analyzing empirical crowdfunding data found that being unbanked* was negatively correlated with crowdfunding adoption. In other words, markets with more developed financial participation (generally, advanced economies) are where the greatest amount of crowdfunding activity is taking place.

Now, what does data from crowdfunding adoption have to do with cryptocurrency adoption?

For one, both are forms of alternative finance, which can be defined as any new financial instrument, channel or system that emerges outside of traditional financial services (e.g., banks, capital markets, etc). What happens in one area of alternative finance may be relevant to other areas, although this relationship needs further exploration.

A second reason why this result may matter for cryptocurrency adoption is that this finding lends support to the fact that already possessing a bank account can reduce on-boarding frictions associated with participating in alternative finance. For example, one of the easiest ways to acquire bitcoin is through a cryptocurrency exchange, and transferring funds into a cryptocurrency exchange can be difficult if not impossible without a bank account.

And, of course, there is the fact that someone who already has resources and savings in an existing bank account will probably also have greater financial wherewithal to participate in crowdfunding or adopt cryptocurrency.

Having said all that, one thing that the paper does not address, and which an earlier paper of mine focused on, is the quality of the financial services available in different countries.

My paper (downloadable here) suggested that those lacking access to quality financial services, as indicated by data on banking and currency crises, sound monetary policy, cost of cross-border transactions, financial repression, and so on, may be relatively more likely to adopt cryptocurrencies such as bitcoin.

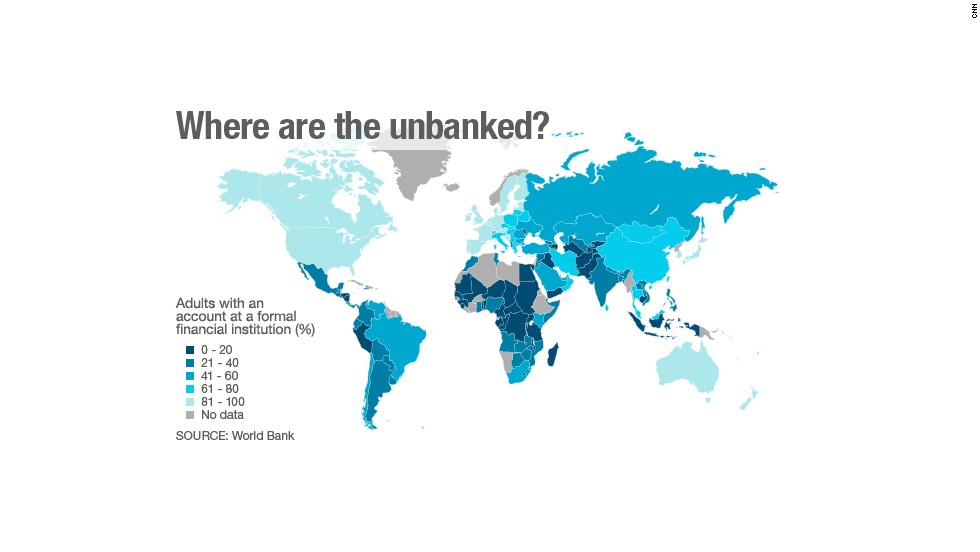

As the regions with relatively low-quality financial services - Sub-Saharan Africa, Latin America, and the former-Soviet countries - are also the same regions with the largest unbanked populations, the question of how likely underbanked regions are to adopt cryptocurrency remains an open question and warrants further study. But certainly one possibility is that it is the already banked - and not the unbanked - within countries with low quality financial services that will be the most likely to adopt cryptocurrencies.

*Note: the term 'unbanked' is represented here by a World Bank measure of the percentage of people in a country that hold an "account at a formal financial institution" such as a "bank, credit union, another financial institution (e.g., cooperative, microfinance institution), or the post office (if applicable) including respondents who reported having a debit card".